Why the Washington Post’s Campaign Against Glass-Steagall?

January 2016

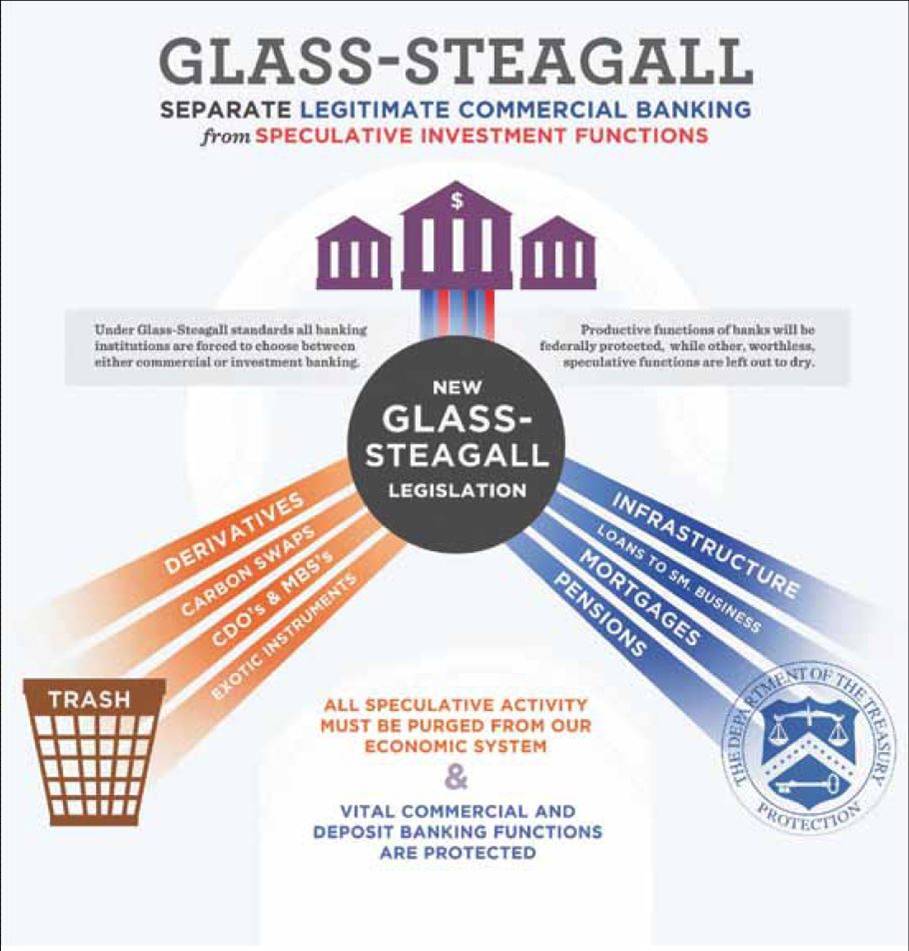

View full size |

Jan. 20, 2016 (EIRNS)—It is astonishing that the Washington Post should run exactly the same, lengthy "Fact Checker" column on two consecutive Sundays—Jan. 10 and Jan. 17—with no explanation, nor even a note on the fact that it was publishing the identical edition of this regular column a second time.

But consider that this column was an attempt to debunk the idea that the Glass-Steagall Act would have stopped Wall Street from causing the 2008 global financial crash. That suggests what the Post is up to, as does regular columnist Catherine Rampell’s furious anti-Glass-Steagall rant Jan. 20, and other pieces in the same vein.

This "Fact Checker" column, by regular author Glenn Kessler, intended to disprove Sen. Bernie Sanders’ widely reported New York speech, asserting that Glass-Steagall would have stopped the big commercial bank holding companies from lending vast sums to "shadow banks"—hedge funds, investment banks, private equity funds, money market mutual funds, etc.—for securities speculation. The activities of those London and Wall Street "non-banks" clearly triggered the 2008 crash, by their wildly leveraged securities and derivatives speculations. But who provided them the leverage?

Washington has been told ad infinitum by President Obama, Tim Geithner, Barney Frank et al. that since Glass-Steagall regulated and limited the activities of commercial banks, it would not have regulated or limited the fatal activities of these shadow banks. That requires believing a fairy tale: that commercial bank holding companies, post Glass-Steagall, did not move trillions of deposit money into securities speculation, by and with "non-banks," blowing up the shadow bank sector until it was larger than the banking sector itself, and inextricably entangled with it. The collapse of one—Lehman—then meant the collapse of all. Eleven of the 12 largest U.S. bank holding companies were insolvent when bailed out in September-October 2008, according to the later testimony of Fed Chairman Ben Bernanke to the Angelides Commission.

The repealed Glass-Steagall Act mandated the following regarding commercial banks and their holding companies:

[Sec. 3 (a)] Each Federal reserve bank shall keep itself informed of the general character and amount of the loans and investments of each of its member banks with a view to ascertaining whether undue use is being made of bank credit for the speculative carrying of or trading in securities, real estate, or commodities, or for any other purpose inconsistent with the maintenance of sound credit conditions;... The chairman of the Federal Reserve Bank shall report to the Federal Reserve Board any such undue use of bank credit by any member bank...." [emphasis added].

Kessler, "checking facts" with various Ivory Tower authorities, seemed not to have checked this section of the law. In his lengthy survey of opinions, he cited only one person, James Rickards, who is actually familiar—from many years’ legal consulting for banks and hedge funds—with the facts of operation of this Glass-Steagall mandate. Rickards’s experience made him crystal clear: He wrote a Forbes column in 2012 titled, "Repealing Glass-Steagall Caused the 2008 Crash." Rickards told Kessler that Fed Chairman Alan Greenspan used a specific Fed rule to give banks exceptional, case-by-case permission to lend to shadow banks despite the Glass-Steagall Act. Greenspan publicly campaigned to kill Glass-Steagall while he was supposed to be enforcing it. After he killed it, banks no longer needed to obtain specific permission from the Fed to violate Glass-Steagall. They then threw their deposit bases, whole hog, into shadow banking and derivatives, and got themselves into serious trouble this way already in 1998-99, with the dangerous derivatives operations of the infamous LTCM hedge fund.

Did the Post run this "Fact Checker" two weeks in a row by mistake? Or, with another crash—worse than 2008—now in early stages, has it joined Wall Street’s "anything, anything but Glass-Steagall" campaign?