This Week in History:

June 5 - 11, 1933

FDR Signs the Gold Standard Act

June 2011

|

|

As the end of the emergency Congressional session, later to be known as the "Hundred Days," approached, President Franklin Delano Roosevelt was engaged in a virtual frenzy of activity, geared toward trying to put credit policy and economic policy on track for a sustained recovery. The Constitutional principle which the President was trying to ram through was clear: The general welfare of the U.S. population had to take priority in guiding the actions of the Federal government.

On June 5, the President took one of his most controversial actions in this direction, by signing the Gold Standard Act. This bill completed the process of freeing the U.S. government from an arbitrary, deflationary gold standard, by abrogating the "gold clause" in public and private contracts, and making legal tender acceptable in settlement of such contracts.

The significance of the series of actions which FDR had taken, which we will review in a minute, was succinctly summarized by author Arthur M. Schlesinger, Jr., in his The Coming of the New Deal. Schlesinger wrote this about the shift away from the gold standard:

"It meant that American monetary policy was no longer to be the quasi-automatic function of an international gold standard; that it was to become instead the instrument of conscious national purpose."

To put it in the language of today's analysis by Lyndon LaRouche: What Roosevelt did was to assert the sovereign right of the nation to control its own credit, rather than permit the "international marketplace" to determine what credit would be available. And he did it because the general welfare of the population depended upon it.

Gold Standard vs. Gold Reserve

Before we get further into our story, it's important to distinguish between two ways of looking at the gold standard: The "British" gold standard, whereby every piece of currency is convertible, vs. the gold-reserve standard, which permits gold to be used as a standard for international valuation, but at a ratio to the currency emitted. In the first, gold basically limits the credit which can be issued, and keeps control in the hands of those with "hard" currency. In the second, gold works as a stabilizer for settling accounts, but the fundamental reality of the fact that it is production, not precious metal, which comprises wealth, is made clear.

What FDR did with his moves on gold, which were followed up in international conferences, up to the Bretton Woods Conference itself, was to move the U.S. from the gold standard—which had been imposed with Specie Resumption back in the 1870s, as a reaction against U.S. sovereign control of currency through the greenbacks—to the gold-reserve standard.

Defense of the Nation

|

|

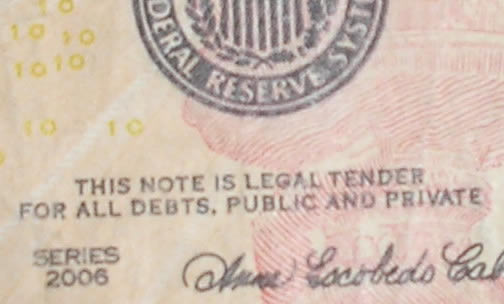

The Gold Standard Act abrogated the "gold clause" from all contracts, so that this paper money became legal for the payment of all debts, public and private (no payment in gold could be legally demanded). |

President Roosevelt took his first measures on gold in the days and months immediately following his March 4, 1933 Inauguration. On March 5, he suspended all transactions in gold, and gave authority over any such matters to the Secretary of the Treasury. On April 5, he went further, issuing an executive order against hoarding of gold.

In the ensuing weeks, acting through Morgan Bank interests in Europe, and the private U.S. banks, including Brown Brothers Harriman, the Bank of England launched an all-out assault on the dollar. The result was an enormous demand for gold to be shipped out of the United States, into Holland and England. New York agents of the British began demanding a lifting of the gold embargo, and an increase in gold shipment licenses.

On April 19, the President called a press conference and announced that, effective that day, he would not permit the "exporting of gold, except earmarked gold for foreign governments ... and balances of commercial exchange."

But this still left the status of gold in limbo. The role of gold was still enshrined in all public and private contracts, as the ultimate means of payment, upon demand. This had an inhibitory effect upon lending, if, as was the case for the majority of those in business and agriculture who were trying to get back on their feet, the borrowers did not have access to gold. In fact, the President and his party were under excruciating political pressure from constituency leaders and their Congressmen, who wanted the loosening of credit, including even the reinstatement of greenbacks, which were used in the time of Abraham Lincoln.

Thus, Roosevelt decided to ignore the screams of the bankers, including "Democrat" Bernard Baruch, and have Congress pass a bill which would remove the last vestiges of the gold standard. The bill passed by an overwhelming majority—and, despite a legal challenge which lasted all the way into 1935—was ultimately upheld. As the first Treasury Secretary of the U.S., Alexander Hamilton, himself had said that public interest must outweigh private market concerns when they conflict: The "general welfare" is the standard.

The original article was published in the EIR Online’s Electronic Intelligence Weekly, as part of an ongoing series on history, with a special emphasis on American history. We are reprinting and updating these articles now to assist our readers in understanding of the American System of Economy.