EIR Editorial

No Solution But To Shut Down Wall Street Now

by Dennis Small

January 2016

A PDF version of this article appears in the January 15, 2016 issue of Executive Intelligence Review (EIR) and is re-published here with permission.

Jan. 11Mass deaths and economic devastation are now on the immediate agenda for the population of the United States, as well as Europe, as the effect of Wall Streets policy as implemented under the Obama Presidency. There is no possibility of keeping people alive, under the present trends of conditions, Lyndon LaRouche warned in a discussion with the LaRouche PAC Policy Committee today, emphasizing that the collapse of the international financial system of which he had warned in mid-December, is fully underway.

LaRouche PAC

Lyndon LaRouche, addressing the Manhattan Project on September 26, 2015. |

Your economic policy of the United States, and of the British Empire in general, demands the immediate mass genocide of the people of the trans-Atlantic community, LaRouche stated. Thats a fact! If we expose that now, we still have a last moment of chance to reverse that effect by shutting down Wall Street and removing Obama from office.

The fact is, that every single dollar of Wall Streets $2 quadrillion speculative bubble is totally worthless, and must be wiped off the books without recompense. Otherwise, under the bail-in policy now being implemented, everything you and your family may havesavings, pensions, food, health care, jobs, homes, everythingwill be seized in the name of protecting the criminal British Empire system which created that speculative bubble.

Therefore, Wall Street has to be shut down now, LaRouche insists, and Franklin Roosevelts Glass-Steagall law reinstated. That then has to be followed up with a supporting action, a Franklin Roosevelt solution, to organize mass funding for people who have lost their sources of income; for people who have been tortured to death by lack of food and the conditions under which they live and work.

The people must also know that theres a hope of reversing the kind of treatment of their employmentor non-employmentwhich is hitting the people today, as in the early 1930s, when Franklin Roosevelt moved in, to give the people a hope of existence.

LaRouche pointed to the actual root of the problem: that people fell for the lie that money is actual wealth, and an entire financial system has been built on that lie. But, money is not something which has a self-evident value. Value depends upon the creative powers of mankind, to make better the conditions of life of mankind.

Death Spiral

LaRouche issued this clarion call to arms on Jan. 11, even as the trans-Atlantic financial system was sinking into a death spiral. In the first week of 2016, global markets crashed by 6.5%, wiping out $4 trillion in worthless paper; the price of oil plunged by 10%, and is now headed to under $30 per barrel; Puerto Rico defaulted on a chunk of its $72 billion debt, which could create a crisis that could quickly spread throughout the entire municipal bond market; and the Jan. 1 activation of the British Empires bail-in policy across Europe is leading to a freezing-up of the bond market, with early indications that even inter-bank lending is seizing up.

Lyndon LaRouche, the worlds leading economic forecaster, had warned in mid-December that precisely this would occur. In a statement that was widely circulated internationally, LaRouche on Dec. 17 warned that the planet stood at the edge of the abyss of a general collapse of the trans-Atlantic system, and that this would strike shortly after the first of this next year. He stated that the British Empires policies under these conditions, especially its bail-in thievery of trillions of dollars of citizens assets, scheduled to go into high gear in Europe on Jan. 1, would unleash genocide on a level not seen since the Fourteenth Century New Dark Age, which wiped out nearly half of the European population. And he warned that this general collapse would happen suddenly, as it now is.

View full size Subscribe to EIR Online http://www.larouchepub.com/eiw |

Do not look for the cause of the crisis in proximate effects, such as Puerto Ricos default, the blow-out of the shale-oil and related bubbles, or in the Federal Reserves incompetent decision to raise interest rates by 0.25% in December. And for sure dont be so imbecilic as to blame China for the meltdown of the trans-Atlantic financial system, supposedly because its GDP growth rate for 2015 came in at only 6.9%, as compared to an expected 7%. Asia, led by China, is the only sector of the world economy which is doing relatively well in physical economic terms today, and will be partiallybut only partiallyshielded from the trans-Atlantic meltdown.

The cause of the financial events now unfolding is to be found in the gargantuan, completely unpayable $2 quadrillion speculative bubble that has built up across all markets since the demise of the Glass-Steagall Law in 1999, and in the underlying belief that money, and money alone, constitutes real wealth. To that, add the concomitant policy of negative economic growth and drastic population reduction, which is the stated policy of the British Empire and of its stooge Obama.

Quantitative Stealing

Take the case of the so-called bail-in policy which went into effect across the European Union on Jan. 1, 2016, and is also fully authorized in the United States under Title II of the criminal Dodd-Frank bill passed by Congress in 2010under excruciating pressure and blackmail from Barack Obama, and in opposition to the Glass-Steagall policy that the concerted campaign of the LaRouche Movement had succeeded in getting placed on Congresss agenda at that time.

Bail-in has been sold to the public as the way to make sure that another Lehman-style 2008 financial crisis never occurs. Instead of using government funds to bail out failing banks through Quantitative Easing and similar hyperinflationary measures, the bankrupt banks purportedly will instead be kept afloat by a bail-in of certain categories of deposits in the banks, and certain categories of bonds of the banks. In other words, depositors and some investors will be expropriated, in order to salvage the cancerous financial bubble. This is what was done in Cyprus when its banks went belly-up in 2013, and it was then promoted as the Cyprus template for all of Europe by Eurogroup President Jeroen Dijsselbloem.

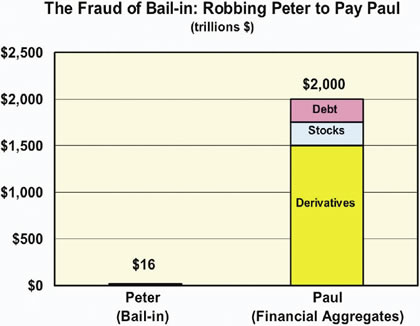

FIGURE 1 |

|

At the time, EIR dubbed the bail-in hoax nothing more than Quantitative Stealing. We also noted that one mans bail-in is another mans bail-out. The crucial question is, what financial instruments are meant to be bailed out, or kept afloat, by the Quantitative Stealing of others? The answer is explicit, in both the EUs guidelines for so-called bank resolution and in Obamas Dodd-Frank law: Derivatives held by the worlds mega-banks are not to be touched, if doing so would create systemic problems for the international financial systemwhich, of course, would be the case in all instances. The plan, in other words, is to rob Peter (you and your family) to pay Paul (Wall Street and the City of London).

But the scheme is absurd even on its own terms. There are about $1.5 quadrillion in financial derivatives in existence, out of a total $2 quadrillion financial bubble. How much loot is available to be bailed in to salvage the derivatives? A mere $16 trillion,[1] scarcely 1% the size of the derivatives bubble that Wall Street intends to rescue! (see Figure 1)

By no stretch of the imagination can this cockamamie scheme work for its stated purpose of salvaging the financial bubble. The only result of Wall Streets bail-in policy in the real world will be to accelerate the onrushing financial meltdown and totally destroy the physical economy and the populations living standard, leading to rapidly accelerating death rates across the planetwhich is precisely the stated intent of the British Empire.

Jail, not Bail

What is now referred to as bail-in used to be called by its proper name: fraud. Back in the 1920s and 1930s, JP Morgan and other banks knowingly defrauded their clients by pushing them to buy shares in their banks, which shortly went belly-up. Some bankers went to jail for the crime back thencourtesy of FDR. A few years ago, Spains major banks, including Banco Santander, pulled the same stunt by selling their own clients so-called preferentes (preferred) shares in the failing banks, saddling their customers with enormous losses.

Earlier this year, in the case of Puerto Rico, some of the worlds largest banks, again including Santander and UBS, were caught red-handed while similarly off-loading bad Puerto Rican municipal bonds from their own books, while at the same time suckering their clients into buying them. And in Italy, four banks were bailed in, in December 2015 by expropriating the holdings in the banks of 10,000 of their clients. The same theft is now beginning in Portugal and other countries, with deadly consequences.

youtube/euronews video grab

A June 2015 rally against austerity in Greece. Southern Europeans are acutely aware of the danger the City of London-Wall Street policy means for their lives. |

And now this fraudulent practice has been codified as not only fully legal under the new bail-in regulations implemented by the European Union as of Jan. 1, 2016, but it is furthermore being required of Europes banks, to sell bail-in bonds (bonds that would be instantly expropriated in the case of the banks insolvency) to the tune of 8% of their total assets. The identical policy was put on the books in the United States with the infamous Dodd-Frank bill, rammed through Congress by Barack Obama with Wall Street money.

The desperate lunacy of the bail-in scheme has many in Europe alarmed. For example, the former head of the Italian Deposit Guarantee Fund (FITD), Paolo Savona, wrote in an article for Milano Finanza in early January that the EU bank resolution mechanism is arbitrary, and guaranteed to fail:

The Guidelines on Resolution of banking crises has the typical features of European Treaties and regulations, which forecast everything except those cases that are really important, in case of major crises . . . I fought against the approved mechanism as long as I was allowed to do it by those who prefer the rule of men to the rule of laws.

Even the City of Londons Financial Times is nervous about what they have unleashed, noting that banks that have been bailed insuch as Portugals Novo Bancohave immediately had their credit rating reduced. That is also expected to happen with any bank that begins to actually market bail-in bonds. Furthermore, the Financial Times admits, smaller banks will be unable to market any bail-in bonds, and will be gobbled up by the already bloated mega-banks. It quotes investment banker Davide Serra saying: This should also trigger consolidation of the smaller banks as a lot of them could be cut out of the bond market.

In fact, no European banks were able to market any bonds whatsoever in the first week of 2016.

The Decisive Battleground

But the decisive battleground, both on bail-in per se and the broader question of the blowout of the world financial system, is the United States. The $2 quadrillion financial bomb must be defused by shutting down Wall Street and declaring all its supposed assets null and void, as Lyndon LaRouche has insisted, and the way to do that is by immediately returning to FDRs Glass-Steagall act. The cowardly Congress should never have left Washington for the Christmas holiday without passing that legislation, but now that they are back in session, their feet must be held to the fire to pass Glass-Steagall as the first order of business.

The Presidential campaign has become a sounding board for the beginnings of a discussion of Glass-Steagall, but that must now become a stampede for action, while it is still possible to prevent the devastation that otherwise awaits us under the British Empire and Obamas rule. It is time to listen to the wise words of Lyndon LaRouche: What you have to do is, pose out the fact that there will be no solution, unless Wall Street is put out of business right now. And thats what Franklin Roosevelt did in effect. He shut down Wall Street.

Footnote:

[1] In the case of the EU, the guidelines that went into effect on Jan. 1 require banks to issue so-called bail-in bonds equal to 8% of their total assets. Bail-in bonds are self-defined as bonds that would be instantly expropriated when a bank becomes insolventin other words, they are rat poison. Leaving aside for a moment who in the world would ever buy such a guaranteed-to-fail financial instrument, the total amount to be issued in the EU is about $2.8 trillion (8% of the $34.5 trillion in bank assets). If a similar approach is taken in Japan and the U.S. (where it is also mandated, under Dodd-Frank), another $1.9 trillion in such bonds would be issued, for a total of $4.7 trillion globally.

If you add to that bail-in amount, the outright seizure and expropriation of bank deposits as was done in Cyprus (about one-third of the total, despite pious promises from EU authorities that deposits of under 100,000 euros would not be touched, promises which were promptly violated), that theoretically would add another $11.8 trillion to the pot of assets to be stolen. So the nominal total bail-in would be slightly over $16 trillionnowhere near enough to salvage the derivatives bubble, but plenty big enough to kill off billions of human beings.