EIR’s Dennis Small illustrates the onset of hyperinflation in this LaRouchePAC TV video dated February 22, available on the LaRouche PAC website..

Financial System on Steroids:

Shut Down the Casino Economy

|

|

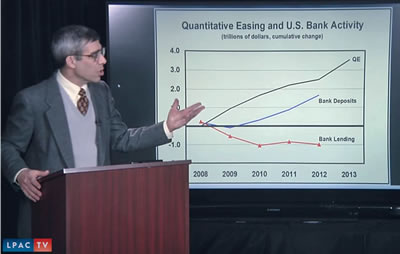

February 22—After the virtually unanimous support for the policy of miraculous multiplication of money—the so-called “quantitative easing” of “Helicopter Ben” Bernanke and European Central Bank (ECB) President Mario Draghi—expressed by the G20 countries at their February 15-16 meeting in Moscow, some representatives of the financial world are getting the jitters. The ultraconservative Swiss newspaper Neue Zürcher Zeitung even mentioned the hitherto taboo H-word (hyperinflation). At the same time, the markets are being flooded not only with money, but also with various ersatz versions of a banking system that would separate commercial from investment banking—all of which only have one purpose: to conceal the speculation and prolong the dancing on the volcano for just a little longer.

On February 18, an article in the Neue Zürcher Zeitung warned that the super-easy money policy makes it only a matter of time before high inflation, or even hyperinflation sets in. Charles Gave of the Hong Kong research firm GaveKal pointed out the real reasons for the impending crisis point: namely that Europe is a huge Potemkin village; behind its facade, Southern Europe is in a death spiral caused by the destruction of the industrial base in Italy, Spain, and France since the introduction of the euro. Two days earlier, the same newspaper attributed the surge in stock prices to “monetary policy steroids,” with reference to Lance Armstrong, the fallen star of the Tour de France. The stock market rally will ultimately prove to be a poisonous gift from the central banks, and the financial house of cards will once again collapse, the paper wrote.

Even if the Zeitung thinks it has to quote other people—investors and analysts—in order to say this, it is still the truth. Southern Europe is indeed in a death spiral. In Greece, for example, people only have access to 268 of 900 essential medicines; the suicide rate is rising throughout southern Europe; a huge brain drain from the South is benefitting Germany and Northern Europe in the short term, but is destroying the foundations for economic recovery in the South: a Potemkin village in Europe, while the financial policy of the entire trans-Atlantic region and Japan is on drugs. The central bankers’ gift of a Trojan Horse makes the mega-speculators happy, while proving disastrous for all.

Lyndon LaRouche warned in his Friday webcast on February 15 , that behind the easy-money policy of the central banks of the U.S., EU, U.K., and Japan, there is a clear intention to let the unpayable debt of the financial system vanish into thin air from hyperinflation, and to expropriate the wealth of large mass of the population, while designing a new currency system only for the benefit of members of the “club” of the international financial elite. That statement may seem shocking at first, but its truth is obvious to anyone who thinks through the “no matter what it costs” policy of ECB chief Draghi & Co., or who has thought about Germany’s hyperinflation of 1923. Then as now, there were war profiteers who benefitted from the hyperinflationary policy by fleeing in time into material assets, industrial plants, mines, etc., and, after the currency reform, strengthened their positions.

Glass-Steagall Is the Way To Go

|

Fortunately, the financial establishment is by no means unanimous regarding this unlimited opening of the monetary floodgates. As the minutes of the latest meeting of the U.S. Federal Reserve’s Open Market Committee (FOMC) on Jan. 29 show, the number of participants who reject Bernanke’s policies is increasing from “some” to “many.” For the first time, there was open discussion of phasing out the hyperinflationary money generation, and of the associated difficulty that this policy means that the Fed would destroy many of its own titles, so that a phase-out is impossible as long as the casino economy is maintained.

Richard Fisher, the Fed chief in Dallas (Texas), and Thomas Hoenig, deputy chairman of the Federal Deposit Insurance Corporation (FDIC), are the leaders of a growing faction of Fed governors, bank regulators, and regional bankers in the U.S. who are working for the full re-establishment of Franklin Roosevelt’s Glass-Steagall Act. This is based on their recognition that the hyperinflation policy of Bernanke & Co. will have catastrophic social, political, and economic consequences.

LaRouche’s Political Action Committee has launched a national campaign for the reinstatement of Glass-Steagall. The most recent success of this mobilization is that South Dakota’s legislature has become the seventh in the country where a resolution has been submitted supporting that policy. Activists are reminding their state legislators, Congressmen, and Senators of their duty to defend the general welfare, as specified in the U.S. Constitution. Given that many parts of the United States are in just as bad shape economically as Southern Europe, this conflict has become hand-to-hand combat between U.S. patriots and Wall Street lobbyists.

Germany: Sticking with Monetarism

So far at least, the situation in Germany is still relatively underdeveloped in this respect. To be sure, the federal government has now presented, in coordination with the French government, one of the many ersatz variations of banking separation, namely its “draft legislation on protection against risks and on planning the reorganization and closing down of banks and financial groups.” But it unfortunately remains completely within the framework of monetarism, even recommending further nesting of the major banks for the purpose of continued speculation, and not even mentioning the term “real economy.”

This draft legislation corresponds exactly to what Richard Fisher has opposed about the Dodd-Frank Act and its so-called Volcker Rule, namely that a completely non-transparent financial sector is made even more problematic by complex regulations, making the situation worse. The German government’s draft law reflects the fact that its authors and their employers do not want to give up speculation and monetarism.

But it is a matter of life and death in the immediate future, to break with this adulation of the monetary system, and to return to a policy that prioritizes the physical economy, as a precondition for the continued existence of mankind. And in the current situation, this can only happen with the full Glass-Steagall separation of the banks, because either money is made available to continue high-risk speculation and gambling, or a credit system will be created exclusively to finance the real economy.

Hyperinflation is already in full swing. It is already visible in asset values, whereas the consumer goods indices are being deliberately manipulated. The explosion of prices for real estate, energy, and food gives a foretaste of what is threatening to explode.

Translated from German by Susan Welsh.

Documentation

Danger of Hyperinflation Breaks into Public Debate

Dallas Federal Resrve President Richard Fisher told Reuters news agency February 21, “I’m not alone anymore” in thinking that the Federal Reserve’s quantitative easing policy is not helping to create jobs.

Fisher hit the Fed’s purchase of $40 billion of mortgage-backed securities each month, along with $45 billion in Treasury bonds (totalling $85 billion/month), ostensibly to push down interest rates: “I just don’t personally feel the need for further mortgage-backed activity, but the majority rules, and I’ve been in the minority on that front. . . . The housing market is even becoming speculative in some places.” Fisher said the Fed’s actions to lower interest rates have “artificially” boosted markets, but “done little for the real economy.”

Fisher said the “wealth effect” of QE3 has not led to the robust employment growth that everyone wants. “The cost, however, is maybe higher than we think, because the more we do, the further into uncharted territory we sail, and how do we get out of it?”

The Wall Street Journal on February 21 headlined its coverage of the just-released minutes of the Federal Open Market Committee’s (FOMC) Jan. 29 meeting “Split on How Long To Keep Cash Spigot Open.”

For the first time, according to the minutes, the potential was openly discussed in the FOMC that if the Fed continues the quantitative easing much longer, it may, when it then attempts to “exit” that policy, wipe out a big chunk of its own capital as a bank. This would result directly from the sharp rise in interest rates these FOMC members now foresee, when and if the Fed starts selling its immense asset book, soon to equal 25% of U.S. GDP. The longer the Fed keeps buying up $85 billion/month in mortgage-backed securities and Treasury securities, the more certain this “exit” interest-rate spike becomes. If Fed asset losses were to wipe out part of its capital in such an “exit” situation, either the Treasury would have to step in with tens of billions more in taxpayer funds as additional capital—bailing out the Fed!—or the Fed itself would have to lurch back in the direction of even more rapid money-printing—or both. In a word, the Fed may soon become unable to exit from the hyperinflationary policy, as many fearful FOMC members are suspecting.

The Journal had reported February 20 that FOMC members were alarmed that the money-printing policy is causing “excessive risk-taking and instability in financial markets.” Bubbles in “junk” corporate bonds and in mortgage-backed securities have zoomed back up again, as in 2005-07.

“Don’t sit on the same hot stove twice,” is the way Richard Fisher put it, as quoted by the newspaper.

Yalman Onaran, in a Bloomberg article titled “U.S. Banks Bigger Than GDP as Accounting Rift Masks Risk,” February 19, quoted from an interview with FDIC vice-chairman Thomas Hoenig who said that “derivatives, like loans, carry risk. To recognize those bets on the balance sheet would give a better picture of the risk exposures that are there.” Hoenig is an advocate of restoring the Glass-Steagall Act (although Bloomberg does not say so).

Onaran reviewed data compiled by Bloomberg that bear out this point, and continued:

“Using international standards for derivatives and consolidating mortgage securitizations, JPMorgan Chase & Co., Bank of America Corp. and Wells Fargo & Co. would double in assets, while Citigroup Inc. would jump 60 percent, third-quarter data show. JPMorgan would swell to $4.5 trillion from $2.3 trillion, leapfrogging London-based HSBC Holdings Plc and Deutsche Bank AG, each with about $2.7 trillion.

“JPMorgan, Bank of America and Citigroup would become the world’s three largest banks and Wells Fargo the sixth-biggest. Their combined assets of $14.7 trillion would equal 93 percent of U.S. gross domestic product last year, the data show. Total assets of the country’s banking system would be 170 percent of economic output, still lower than 326 percent for Germany.

“U.S. accounting rules for netting derivatives allow banks to erase about $4 trillion in assets, the data show. The lenders also can remove from their books most mortgages they package into securities, trimming an additional $3 trillion.”